The Importance of Valuation: How to Avoid Running Afoul of RESPA’s Anti-Kickback Provisions

August 15, 2017

By Jon P. Klerowski

While part one of this article provided an overview of the legal and compliance climate surrounding RESPA’s prohibitions against kickbacks and referral fees, part two provides recommendations on how to support and document fair value determinations to avoid risk of non-compliance.

Fair value analyses—conducted contemporaneously with the execution of an agreement or transaction—are a critical aspect of RESPA Section 8 compliance as they can demonstrate that (i) any payment for compensable services rendered is reasonably related to the value of those services, and (ii) any payment related to ownership interests of an ABA is at fair market value of the interest being bought or sold. Although the CFPB undertakes a thorough and critical review of valuation methodologies when it does choose to consider a RESPA 8(c) exception analysis, the fact remains that there are widely-used and accepted valuation approaches which can support value determinations.

Below we use accepted valuation concepts and describe an appropriate methodology to (i) value services to demonstrate that when payments are made, they are appropriate and reasonable given the services performed, and (ii) determine the fair value of the ownership interests of an ABA that may be bought and sold. In so doing, we note that while fair market value may not always be precise, a relatively narrow range can be determined. Importantly, the fair value analyses are more supportable in the current regulatory environment when the following legal principles are considered:

- A settlement service provider should not pay more than fair market value for marketing services or ownership interests in a service business if the provider is able to receive referrals from the marketer or the business. This is because the excess would be a “thing of value” and if the marketer or the business that is purchased has a pattern of sending business to the provider, there could be an inference that the payments were excessive to compensate for referrals. In that instance, both the giver and receiver could be equally liable.

- Likewise, a settlement service provider should not offer free or below market rate services to a person in a position to make referrals to that provider. The free or subsidized services would be a “thing of value” that could be scrutinized as being given in exchange for referrals. It then follows that persons in a position to make referrals and who expect to do so should not agree to receive excessive payments, discounted services, or other things of value as that would also raise an inference of compensation for referrals.

Thus, keeping in mind these points of sensitivity, standard valuation techniques can be applied to demonstrate value relating to the various RESPA scenarios that industry participants typically confront.

Valuation Methodology for Service Agreements

Service Agreement Background

Service Agreements are arrangements between real estate settlement service providers where one party provides marketing services for another (typically a real estate agent or broker provides services for other settlement service providers such as mortgage lenders or title insurance). Service Agreements generally include a wide-range of marketing services in exchange for a monthly fee. Typical services include:

- Mailings: Email and direct mail marketing campaigns.

- Web-based advertising: Banner advertisements or website links displayed on the marketer’s website.

- Signage: Displays at real estate sales offices, real estate listings or other locations.

- Provision of other materials: Brochures, flyers, business cards, and other printed materials.

Additional less-common services include providing office space, consulting, sponsorships and work-share agreements, which typically involve subcontracting part of the services one entity provides to another service provider

Valuation Approach

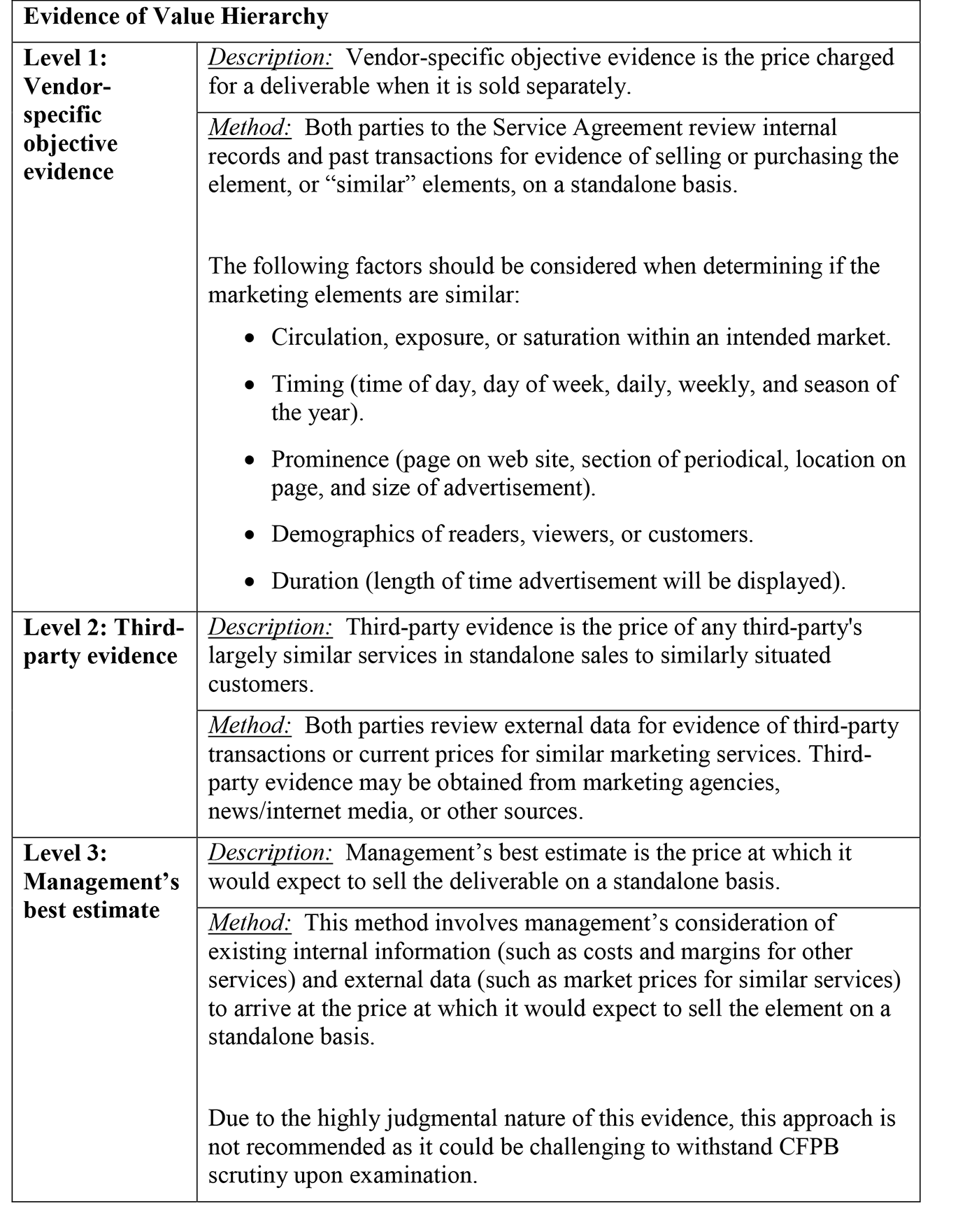

As Service Agreements usually have multiple services (or elements) exchanged for a stated fee, the main concern is determining the value of each element to ensure that the total payments are commensurate with the services provided. Generally accepted financial reporting standards provide guidance for valuing arrangements with multiple deliverables in ASC 605-25, Multiple Element Arrangements. This GAAP reporting standard provides a relevant framework for measuring and allocating arrangement consideration amongst the various deliverables based on a hierarchy of available evidence for each element’s standalone value. The hierarchy in ASC 605-25 is as follows:

- Vendor-specific objective evidence

- Third-party evidence

- Management’s best estimate

An approach using a similar hierarchy to demonstrate value can be applied to the multiple elements of Service Agreements. Notably, while the valuation approach described in greater detail below is rooted in GAAP, it is also consistent with the standard business valuation technique known as the market approach. Put simply, the market approach utilizes observable factual evidence of arm’s length transactions to derive indications of value. Similarly, the valuation approach applied to Service Agreements compares each service element to similar observable market evidence to derive value.

Valuation Approach Applied to Service Agreements

As is typical with most Service Agreements, the approach described below assumes a stated monthly fee in exchange for multiple types of services; however, the concepts and methodology can be tailored to apply to other fee structures as well.

Step 1 – Apply the ASC 605-25 evidence hierarchy to determine each element’s standalone value:

First, determine the distinct services (elements) to be provided under the Service Agreement. Then, apply the ASC 605-25 evidence hierarchy to each element to obtain the highest-level evidence of value (i.e. if vendor-specific objective evidence exists, it must be used). Each level of the evidence hierarchy is described in more detail in the table below.

Step 2 – Measure the expected volume of services to estimate the total value of services to be provided:

Once the estimated value for each element has been determined, the next step is to estimate the volume of services to be provided. At this point, the estimated value for each element can be calculated as the per unit value multiplied by the expected volume. For example, suppose that a Service Agreement calls for two email marketing campaigns per month, and vendor-specific objective evidence suggests that an email campaign of that particular nature is worth $5,000. The estimated monthly value for the email campaign is $10,000.

Next, the estimated value for each element would be summed to arrive at the Service Agreement’s total estimated monthly value. This value estimation process should be conducted with input from both parties prior to establishing the monthly fee in the Service Agreement (the expected volume should be documented as well). It is advisable to set the agreed-upon monthly fee below the expected value due to the judgments and estimates used in the valuation process, and for potential instances where the volume of services provided is less than anticipated. Setting the monthly fee below the expected value can also reduce the risks associated with the appearance of kickbacks or referral fees.

Step 3 – Monitoring activities and value reassessment:

The final step in the valuation approach is the ongoing monitoring of services and reassessment of value.

This essential step entails regularly obtaining tangible supporting evidence for services performed, along with the associated activity levels. Examples of supporting evidence include: screenshots of web-based advertising with timestamps, requiring marketers to “CC” on email campaigns, or a monthly written statement of services provided. Once the evidence is gathered, the value of the services provided should be tabulated to confirm that the value provided is greater than the monthly fee. This process of obtaining supporting evidence is necessary to ensure that the monthly fees are a quid pro quo for the volume of services provided and mitigates the appearance of kickbacks or referral fees.

The estimated value for each element should be reassessed periodically to monitor changes that may impact the valuation analysis. The reassessment should occur at least annually, or upon a material change in the services provided or marketplace.

Valuing Ownership Interests in ABAs

Under RESPA, an ABA is a business arrangement in which at least one owner of a real estate settlement service provider directly or indirectly causes a referral of business to that provider and shares in the resulting profits. ABAs present important valuation issues not only when there is an exchange of a thing of value with an owner who is in a position to refer business to the joint venture (or receive business from the joint venture), but also if there is a purchase of an ownership interest in an existing real estate settlement provider with an earnings track record. (When an ABA is first established and is capitalized with cash payments, as is often the case, few valuation issues are presented. However, when an ABA is established with non-cash assets contributed by each party, the fair value of the contributed assets must also be analyzed.) In the latter case, there are three generally accepted valuation approaches which can be used to determine the fair value of the ownership stake: the income approach, market approach and asset approach. Notably, these approaches are interrelated and not independent of each other.

The general concept of the income approach is that the value of a business, business interest, or asset is the sum of the expected future benefits discounted back to a present value at an appropriate discount rate. Thus, the two most important inputs of an income approach analysis are (i) projected future benefits (typically net cash flow), and (ii) a discount rate appropriate for the expected risk of the future income stream. Importantly, this approach can be applied to both controlling and noncontrolling interests, which makes it quite useful in valuing ownership stakes in ABAs.

The market approach uses observable market data for prices of other similar companies (or interests in companies) to derive indications of value—typically data regarding stock prices of public companies or merger and acquisition prices of entire companies (or divisions of companies). When using this approach, it is important to ensure that only arm’s-length transactions are considered for the comparison, reflecting that the buyers and sellers were acting in their own self-interest. If there are sufficient, comparable public companies or arm’s-length transactions to consider, the market approach provides a useful framework for valuing ownership interests in ABAs.

The asset approach is based on the premise that the value of a business can be associated with the productive assets of a business. The basic premise is that the value of a business is equal to the difference between the fair market value of its assets and liabilities. The asset approach is most relevant to asset intensive companies and holding companies, whereas most ABAs are setup as service or operating companies which generally get the bulk of their value from intangible assets such as brand names, trademarks or customer lists. These types of businesses are generally valued using the income or market approach due to their ability to generate earnings and cash flow. However, the asset approach may still be useful because it can provide a value for the net tangible assets contributed to a joint venture.

Each of the three approaches described above should be considered when valuing ABA transactions, including establishing joint ventures and buying or selling ownership interests. Similar to demonstrating value for the multiple elements of Service Agreements, the most important aspect of the valuation analysis under any approach is obtaining evidentiary support and documenting assumptions in order to demonstrate value contemporaneously with the execution of any ownership transaction or establishment of a joint venture.

In Summary

Due to the CFPB’s continued focus on RESPA’s prohibition of kickbacks and referral fees, industry participants must pay particular attention to arrangements that are most susceptible to Section 8 scrutiny: Service Agreements and ABAs. Importantly, supportable fair value analyses (conducted contemporaneously with the execution of an agreement or transaction) are a critical aspect of RESPA Section 8 compliance as they can demonstrate that (i) any payment for compensable services rendered is reasonably related to the value of those services, and (ii) any payment related to ownership interests of an ABA is at fair market value of the interest being bought or sold.

Service Agreements and ABAs have inherent legal and compliance risk due to RESPA’s restrictions on mortgage and real estate industry participants providing or accepting kickbacks and referral fees. However, properly executed Services Agreements and ABAs are mutually beneficial to settlement service providers and real estate agents alike. The valuation approaches described above, along with the necessary supporting documentation and monitoring, provide a framework for establishing Service Agreement programs and ABAs where the benefits are preserved and the RESPA compliance risks are mitigated.

Jon P. Klerowski is a principal at PKF O'Connor Davies Advisory LLC, a firm that offers accounting, tax and advisory services. He has significant experience advising executive management, boards of directors, and their counsel on a wide array of accounting, financial reporting and modeling, business valuation and forensic accounting matters. Klerowski acknowledges Marcus B. Hemenway and Derek J. Miller for their contributions to this analysis.

Contact ALTA at 202-296-3671 or [email protected].