Why This Matters

Featured Resources

Legislation

Legislation

Protecting America's Property Rights Act (H.R. 3206)

The Protecting America’s Property Rights Act would require that all products used to insure title risk on federally backed mortgages be properly regulated at the state level, ensuring consumers understand the coverage and pricing of the products protecting their largest investment. You can find a list of cosponsors here.

Research

Research

How Title Insurance Protects Property Rights and the U.S. Real Estate Economy

This First American FAQ explains how the title acceptance pilot would remove lender’s title insurance requirements for certain refinance loans, while underscoring why title defects, lien priority and property rights protections remain critical considerations for homeowners, lenders and the broader real estate market.

Model Resolution

Model Resolution

ALEC Resolution Supporting State-Based Title Insurance Regulation

This model resolution from the American Legislative Exchange Council (ALEC) supports state-based title insurance regulation and warns against federal actions that could weaken oversight. It raises concerns about the Title Acceptance Pilot, attorney opinion letters and other alternatives that may shift risk outside the regulated title insurance framework.

Advocacy & Policy

Protecting Americas Property Rights Act One Pager

This one-pager explains H.R. 3206, which would require mortgages purchased by Fannie Mae and Freddie Mac to be insured against title risk by a state-regulated product, such as title insurance. It warns that alternatives like attorney opinion letters may create consumer protection gaps, reduce transparency and increase financial risk for homebuyers and lenders.

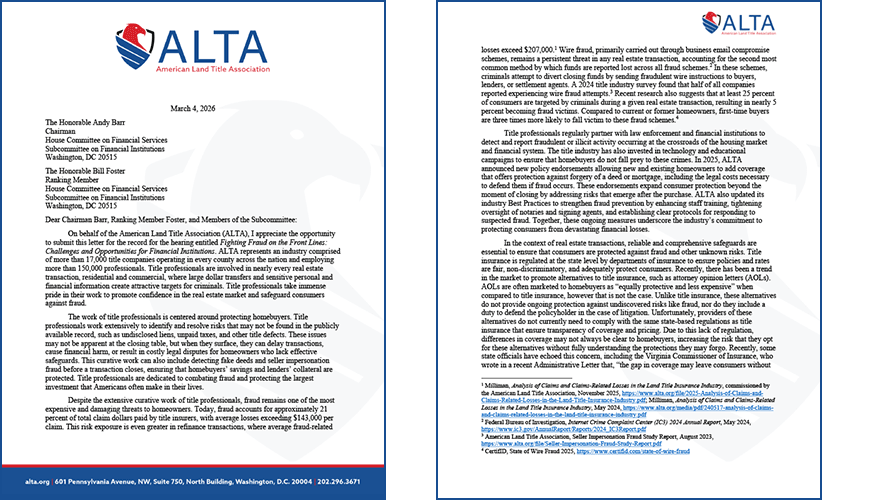

ALTA Letter for HFSC Hearing on Fighting Fraud

ALTA’s letter to the House Financial Services Committee highlights the role title professionals play in fighting real estate fraud and protecting consumers. It also warns that unregulated title insurance alternatives may create coverage gaps and increase risk for homeowners and lenders.

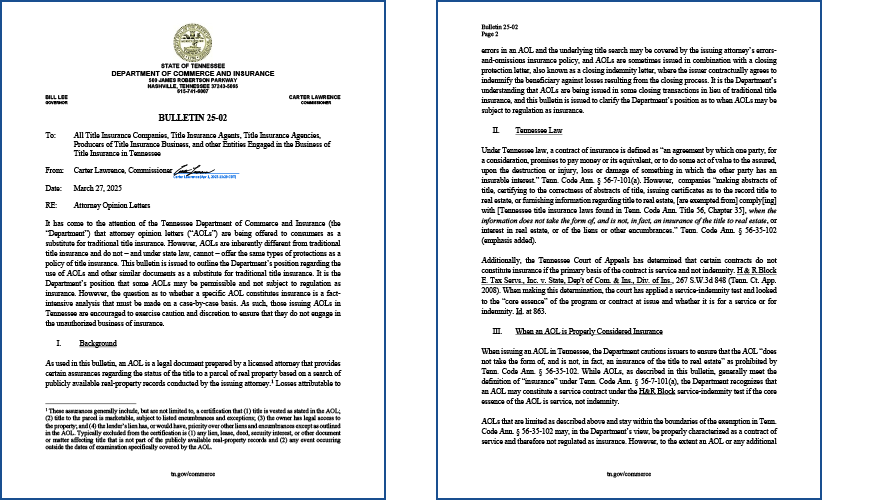

Tennessee Bulletin on Attorney Opinion Letters

This bulletin from the Tennessee Department of Commerce and Insurance explains that attorney opinion letters are different from title insurance and may not offer the same protections. It cautions that some AOLs could be treated as insurance under Tennessee law if they indemnify against title-related losses or function as a substitute for title insurance.

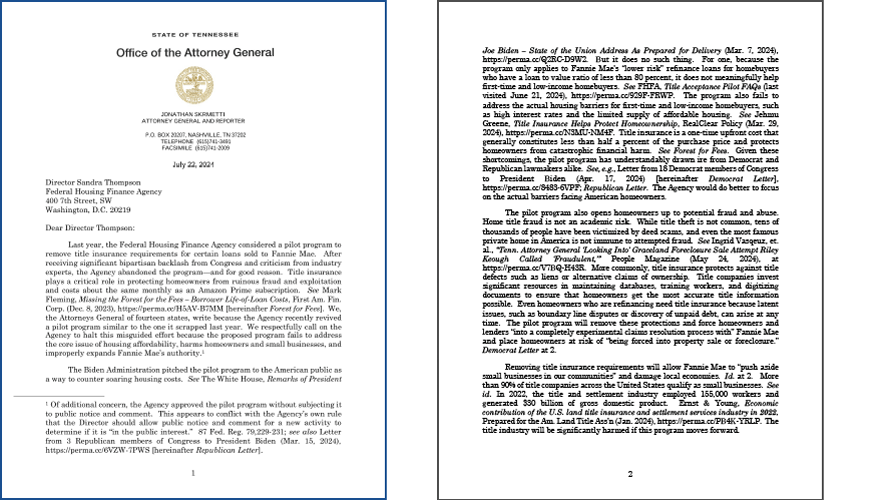

State Attorneys General Letter Opposing FHFA Title Waiver Pilot

This letter from 14 state attorneys general urges FHFA to halt the Title Acceptance Pilot, arguing that it would not meaningfully address housing affordability and could expose homeowners and lenders to greater title risk. The letter also warns that shifting risk away from state-regulated title insurance could weaken consumer protections and harm small businesses in the title industry.

Resources & Tools

Understanding Title Insurance and Its Benefits

This document explains how title insurance protects homeowners and lenders by addressing title defects, fraud, forgery and other risks that may not appear in public records. It also outlines how title professionals support safe closings, perform curative work and provide long-term protection through owner’s and lender’s policies.

Unregulated Title Insurance Alternatives: Risks to Homeowners and Lenders

This resource explains how unregulated title insurance alternatives may expose homeowners and lenders to risks title insurance is designed to cover. It highlights gaps around public records, fraud, legal defense, pricing and regulatory oversight.

News & Insights

Opinion: Congress Should Protect Property Rights, Not Shift Title Risk to Consumers and Lenders

In this op-ed, ALTA CEO Chris Morton urges Congress to pass the Protecting America’s Property Rights Act. Chris warns that weakening title insurance protections or relying on unregulated alternatives could shift hidden legal, fraud and title risks onto consumers, lenders and taxpayers. True housing affordability must include secure property rights and strong, state-regulated safeguards that protect homeowners before and after closing.

Virginia Insurance Commissioner Issues Warning About AOLs

In a letter on Sept. 9, Virginia Commissioner of Insurance Scott White warned consumers and companies offering title insurance alternatives such as attorney opinion letters (AOLs) that these products are prohibited from providing the same or similar protections as title insurance. The bureau advises entities issuing AOLs in Virginia to exercise caution to ensure that they avoid engaging in the business of insurance.

Utah Regulator Revokes Title Company License for Closing Deals With AOLs

The Utah Insurance Department on July 14 revoked the license of a title company for numerous violations, including closing transactions through the UWM Trac Loan program and accepting attorney opinion letters (AOLs) in lieu of lender’s policies.

Attorney Opinions Don’t Count

The federal government continues to push proposals that would dangerously expose lenders and taxpayers to additional risk. In March, the Biden Administration released plans during the State of the Union to revive a previously discredited and shelved pilot program that would waive the requirement for lender’s title insurance on certain refinances.

Title Insurance Matters. Here’s Why.

Without a title insurance policy, homeowners can find themselves fighting for their property over issues they never knew existed. ALTA CEO Diane Tomb shares several examples of how title insurance protects consumers.

18 House Democrats Question Biden Administration’s Title Waiver Program

A group of 18 Democratic members of Congress sent a letter to President Biden expressing concern with the administration’s program that will waive the requirement for lender’s title insurance on certain refinances.

Questions to Consider if Lender Asks You to Close an AOL Deal

Title and settlement agents may see lender customers request a transaction be closed with an attorney opinion letter (AOL) now that Fannie Mae expanded the use of AOLs in limited circumstances for loans on condo properties and those subject to homeowner associations. Read on items you should be considering and questions you should be asking.

White House Title Insurance Waiver Program Would Hurt Wyoming Residents

ALTA member Sasha Johnston, owner of Sheridan County Title in Wyoming, explains why the Biden Administration's title insurance waiver pilot program would be disastrous for Wyoming homeowners and the broader housing finance system.